Summary

The housing boom has lasted longer than housing bears have expected, with shares of homebuilders seeing significant gains.

The iShares Home Construction ETF is up 33% for the year and SPDR S&P Homebuilders ETF has a 27% YTD return.

Why won’t the housing market turn when every economic indicator says it should? I’d argue that new home sales have held up largely because of homebuilders offering buyers teaser rates.

Homebuilders are using short-term mortgage buydowns to attract buyers, but this could lead to chaos as payments automatically reset to higher amounts. This is particularly risky for jumbo mortgages.

I estimate that 600,000 to 700,000 households could face rate resets in the next year, which could quietly put pressure on the economy and housing market.

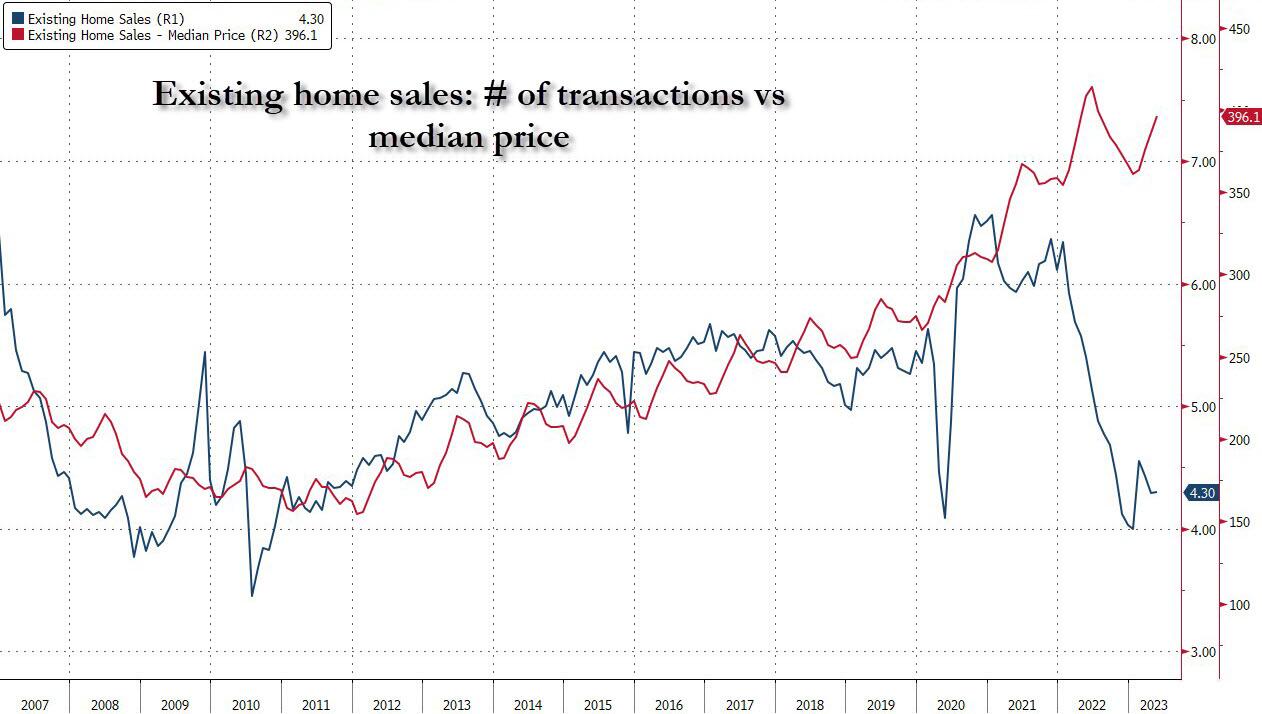

Recent data shows what was a surprisingly strong spring selling season for homebuilders and an existing home sales market that has rebounded in price, even amidst plunging volumes. For shares of homebuilders, this means that the pandemic boom in new construction has carried on longer than most analysts thought it would. The iShares Home Construction ETF (BATS:ITB) is up roughly 33% for the year, and the SPDR S&P Homebuilders ETF (NYSEARCA:XHB) also clocks in at a 27% YTD return. Over the full business cycle, however, publicly traded homebuilders are lousy businesses. Homebuilders are highly leveraged, highly cyclical businesses. Historically, they’ve had poor returns on capital compared with the market at large and tend to go bust during recessions– a fact that is somewhat hidden by survivorship bias when looking at historical returns.

More recently in 2022, this led to the question of whether homebuilders trading for 5x peak earnings or so were good value investments or value traps. I’ve repeatedly taken the position that they’re value traps, but now here we are with homebuilder stocks having rocketed back to all-time highs since the October lows, along with many of the most speculative corners of the market.

The one factor that I massively underestimated was the prevalence of short-term mortgage rate buydowns provided by homebuilders. How these typically work is that builders will buy down borrowers’ mortgage rates for 1-3 years, at which point the mortgage resets to a higher monthly payment. Common forms include 3-2-1 (i.e. 3% reduction in interest in year 1, 2% in year 2, and 1% in year 3), and 2-1.

Research shows that around 75% of builders are using them, with the greatest concentrations of use in Texas and the Southwest. On a $500,000 loan with a 2-1 and prevailing mortgage rates at 7%, the monthly payment would be $2,684 in year 1, $2,997 in year 2, and $3,326 in year 3. By and large, this allowed builders to sell homes that would have piled up by offering teaser payments that reset to levels that are technically legal, but often at rather uncomfortable debt-to-income ratios when combined with property tax increases and skyrocketing utility bills. Throw in some cheap construction and 110-degree summer temperatures, and you have a recipe for potential regret, especially for out-of-state buyers.

Fannie Mae and Freddie Mac restrict buydowns that exceed these thresholds (because of the potential for fraud and abuse), but highly publicized troubles at lenders like First Republic (OTCPK:FRCB) show that the jumbo market has seen some more exotic underwriting. The unspoken implication here is that lenders, real estate agents, and builders are selling these to buyers with the implicit or explicit suggestion that they should refinance down the road and lower their payments, (a.k.a. the infamous “date the rate, marry the house” sales pitch). That works if interest rates go down, but interest rates have actually gone up and the Treasury now has a boatload of deficit-financed debt to sell, which threatens to push mortgage rates above 8% by late summer. Fannie Mae and Freddie Mac at least force buyers to qualify for the payments after they reset, but it’s not clear whether the jumbo market has the same level of protection.

Mortgage buydowns may be innovative for builders, but they’re not newly invented. One of the untold stories of the 2008 financial crisis was the role that homebuilder rate incentives had in fueling the crisis. Adjustable rate mortgages get all the attention for massive balloon payments, but the story in jumbo mortgages was actually quite similar. Many, many buyers who bought in 2005 and 2006 had their mortgages reset in 2008 and 2009 after their rate buydowns expired, and their assumptions about mortgage rates turned out to be wildly wrong. In fact, jumbo mortgage rates hit nearly 8% in early 2009. That’s because jumbo mortgages are heavily dependent on credit, which rapidly tightened then starting in 2007 and also is tightening now. Only after the economy recovered did mortgages start to get cheaper again.

This means that taking out a jumbo mortgage because you think you can refinance it later is riskier than you think! It’s smart for homebuilders to offer these and it extended the business cycle long enough for investors to make profits. However, these rate resets are potentially disastrous for buyers making huge economic bets with scarce information about whether they’ll truly be able to refinance for cheaper rates.

Jumbo Mortgage Rates- 2007-2013

Different data sources on mortgages will generally show slightly different numbers, the main reason being that many mortgage rate surveys don’t count points charged to acquire the loan. But jumbo mortgage rates rose in the early stages of the 2000 recession. And throughout the 2008 recession, we see here that jumbo mortgages actually rose significantly.

So how many people have these rate buydowns? A minority of builders do buy the rate down for the whole 30-year term and a few buyers pay cash, so I think a fair estimate is that roughly 50% of new home buyers have rate buydowns that are 3-2-1 or faster. Roughly 600,000 new homes were sold in 2022, and this year is tracking for about 800,000. Divide by two, and we can ballpark that maybe 600,000 to 700,000 households have rate reset balloon payments coming due over the next couple of years. It may not sound like much, but that’s a figure roughly equal to all of the homes in the US currently listed for sale. Since housing supply for sale is low compared to the size of the overall housing stock, it could change the supply/demand dynamics considerably. My guess is that this will start to quietly become a problem for new homeowners, as we’re just now starting to see rates reset from last summer when mortgage rates first hit 6%.

For jumbo buyers, these can amount to payment hikes of $1,000 to $2,000 per month. Jumbo buyers aren’t likely to get much sympathy from the Fed or Treasury either, as encouraging marginal holders to sell is part of the process of bringing supply and demand back into balance. The strategy of taking out a mortgage and trying to refinance is somewhat better for those buying lower-priced homes with conventional mortgages. At lower mortgage amounts, the government is more likely to intervene to help you if things go south. Still, I wouldn’t expect a whole lot of help without unemployment rising sharply, in which case many buyers will need to sell anyway, driving down prices. Now add student loans restarting, with 40 million borrowers affected. Interesting times indeed.

The Cure For High Prices Is High Prices

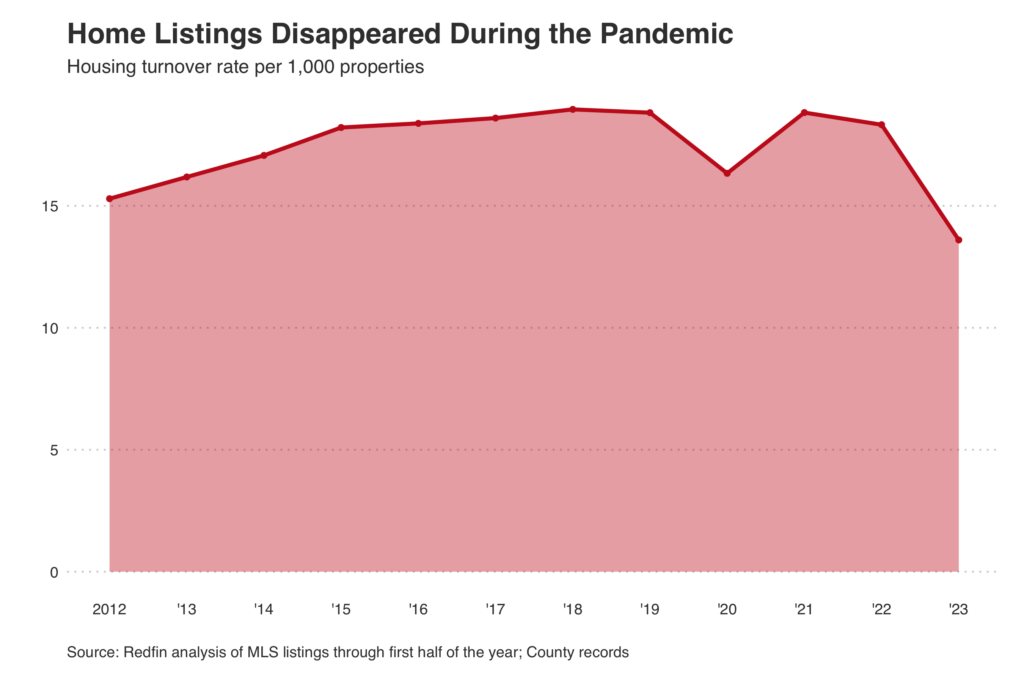

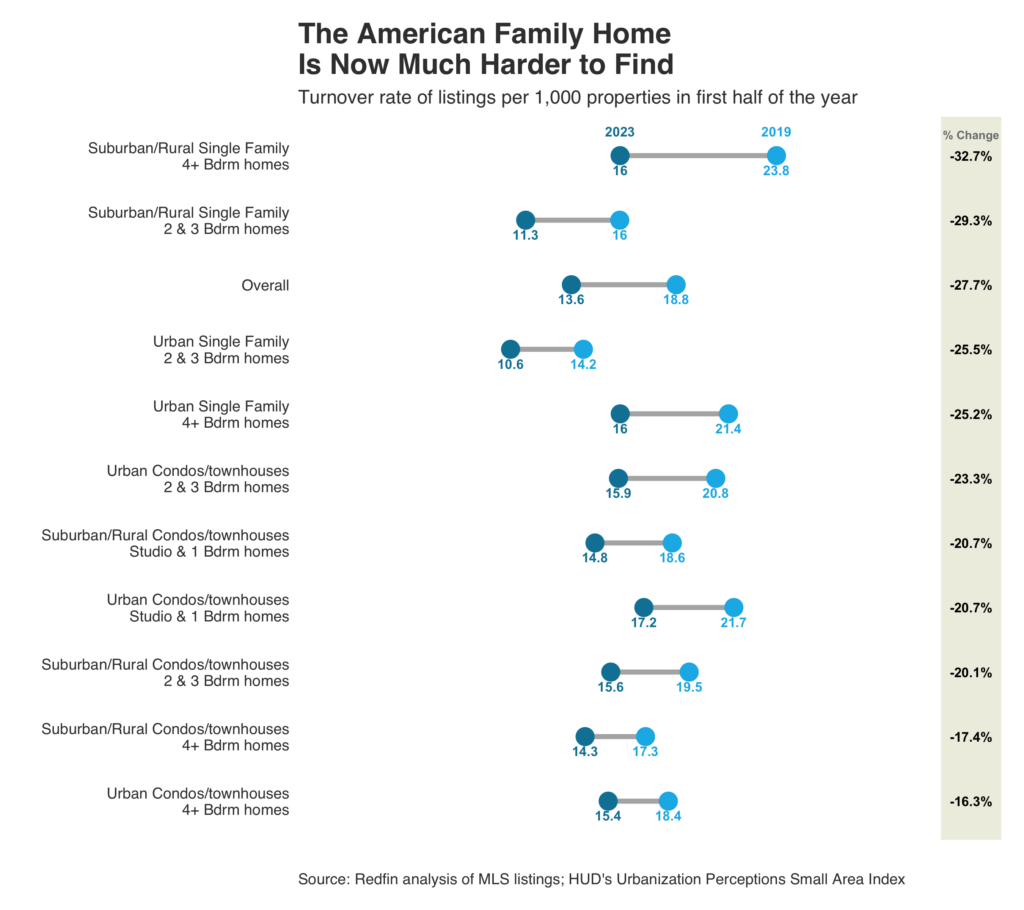

While homebuilders have done well, the looming oversupply in rental housing and falling margins for homebuilders will continue to accelerate. If current trends hold, new homes could soon be cheaper than existing homes, which almost never happens. Builders are aggressively discounting homes, including using rate buydowns, and it’s allowing them to offload houses.

But as a recent report from Reventure Consulting shows, much of this new construction is far out from existing cities, which may help explain why there has been relatively little pressure on the existing home sales market so far. For example, this is a map of new construction in North Texas, where much of the new construction is an hour or longer drive to the city itself. In the 2008 real estate bubble, these kinds of homes were the hardest hit, particularly in areas like Arizona, Las Vegas, and the Inland Empire of California.

But with the median prices of new homes falling from $497,000 at the pandemic peak to $416,000, it’s only a matter of time before buyers start responding in earnest to the market signal they’re being given. As prices for new construction continue to fall, it’s going to pressure the existing home sales market because the two are nearly perfect substitutes. And ask yourself, with new home prices already falling to near the levels of existing homes, who’s going to buy the next 1.7 million units under construction, and at mortgage rates of 7% or more?

Homebuilders clearly had some hefty profit margins to work with in 2022 when they began discounting inventory. But the next 1.7 million houses under construction will be a much tougher proposition to sell or rent. Rents are now falling, interest rates continue rising, and there’s little long-term demographic demand for housing in excess of what’s already been pulled forward. While housing market bears may have been early in calling a downturn, underlying demographic trends likely mean they won’t be wrong about the ultimate destination.

With these in mind, I’m highly skeptical of stocks like Lennar (LEN) now trading for 10.5x earnings, D.R. Horton (DHI) trading for 11.5x earnings, and even from Toll Brothers (TOL) trading for 7.8x. If builders want to buy down mortgages for the full 30-year term for borrowers it’s fine, but doing so affects margins similarly to how price cuts would. When most of the industry is offering short-term teaser rates to new home buyers, the very clear risk is that the houses they sell come back onto the market when the mortgages reset, just like they did in the 2000s, but on a smaller scale. This, combined with the massive wave of construction hitting the market means homebuilder profit margins likely won’t stop falling when they hit 0%.

Key Takeaways

The housing market has been surprisingly strong in 2023, despite the ratio of a typical mortgage payment to a typical wage reaching a level surpassing the 2000s housing bubble.

One reason that the housing market hasn’t turned down as sharply as feared may be due to widespread mortgage rate buydowns by builders.

Many buyers are rolling the dice and betting that they can refinance in a couple of years for a lower interest rate before their payments reset, but jumbo mortgage rates in particular tend to rise, not fall during a recession.

Will home buyers who bought in 2022 with mortgage buydowns sell en masse when their payments reset this year and next? We’ll see.

It remains to be seen whether the economy will achieve a soft landing, but the widespread existence and adoption of mortgage rate buydowns are likely to exacerbate the swings of the business cycle. Count this as one more data point suggesting a soft landing is less likely than pundits think.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Source : https://seekingalpha.com/article/4617622-us-homebuilder-mortgage-rate-buydowns-starting-to-expire

{kind=link}

{kind=link}

{kind=link}